Download the report

Executive Summary

Key Findings

|

Cement manufacturing is one of the most energy- and carbon-intensive industries in the world, contributing around 7% of global carbon dioxide emissions (i.e., more than the food, beverage, paper, and non-ferrous metals industries combined). Cement is a key ingredient in concrete, the widely used building material, and its production will continue to rise globally in the coming years, especially in the global south. Decarbonizing the cement sector will therefore be essential to achieving the objectives of the Paris Climate Agreement, under which the world’s countries committed to reduce their greenhouse gas emissions to net zero by 2050.

This report evaluates the potential of limestone calcined clay cement as a sustainable alternative to portland cement in the United States. We estimate the carbon reduction potential of different adoption rates (10%, 20%, 30%, and 50%) of limestone calcined clay cement by government and private cement users in the U.S. market in 2021, highlight the opportunity to realize these emissions reductions by shifting cement purchases for public construction projects, identify barriers, and offer recommendations to increase adoption.

Compared to portland cement, limestone calcined clay cement reduces emissions, performs as well, and is more cost effective (25%) due to savings in energy and materials

Cement is manufactured by heating limestone to a high temperature to create lime and carbon dioxide. The lime is further heated to produce clinker (an intermediate product), which is mixed with other materials to produce portland cement. Cement, a key binding agent, is mixed with aggregate and water to produce concrete, a widely used building material.

The CO2 emissions from the cement industry can be reduced by (IEA and WBCSD 2018, Goldman et al. 2023):

- Improving energy efficiency.

- Improving material efficiency (e.g., by replacing portland clinker to produce blended cements, substituting portland cement with supplementary cementitious materials (SCMs) to produce concrete).

- Using alternative binding materials.

- Switching from traditional fuels to alternative fuels.

- Using decarbonized, alternative raw materials, and feedstocks.

- Using electrochemical production processes.

- Implementing carbon capture and storage.

Calcined clays represent a material efficiency approach that offers one of the best decarbonization opportunities for the sector, with substantial reductions in new carbon emissions possible, especially when combined with other decarbonization approaches like increased energy efficiency and electrification. Calcined clays can be combined with limestone and used to produce blended cements or be used as an SCM instead of portland cement in concrete. Calcined clays can use existing equipment, such as rotary kilns, reducing capital expenses, and they already enjoy acceptance in the standards community.

Limestone calcined clay cement is a low-carbon replacement for portland cement and can reduce CO2 emissions by up to 40%, under the current state of technology development. It has undergone rigorous testing and been shown to perform as well as portland cement, while costing 25% less to produce due to savings in energy and material use. In addition, it offers adequate mechanical qualities (e.g., durability), making it appropriate for a variety of structural applications, including pavements, highways, residential and commercial buildings, and other infrastructure.

Limestone calcined clay cement is globally scalable. The use of limestone calcined clay cement has been studied in several countries around the world, including India, Brazil, Colombia, and Cameroon. This report discusses case studies from seven countries. Overall, limestone calcined clay cement is projected to account for more than one-quarter of cement use in the world by 2050 (IEA and WBCSD 2018). In the United States, the use of calcined clays has been very limited despite abundant clay deposits in many regions of the country, but there is growing interest.

U.S. CO2 emissions can be reduced by 7.3 Mt annually by shifting half of federal, state, and local government procurement toward limestone calcined clay cement. This is equivalent to eliminating greenhouse gas emissions from driving 1.7 million gasoline-powered cars annually.

The United States is the fourth-largest producer of cement in the world, producing about 91 Mt of portland cement and masonry cement in 2023 (USGS 2024). Sales of cement in 2023 were around $16 billion (USGS 2024). At the state level, Texas, Missouri, California, and Florida have the highest cement production, in that order, and Texas, California, and Florida consume the most cement (USGS 2024).

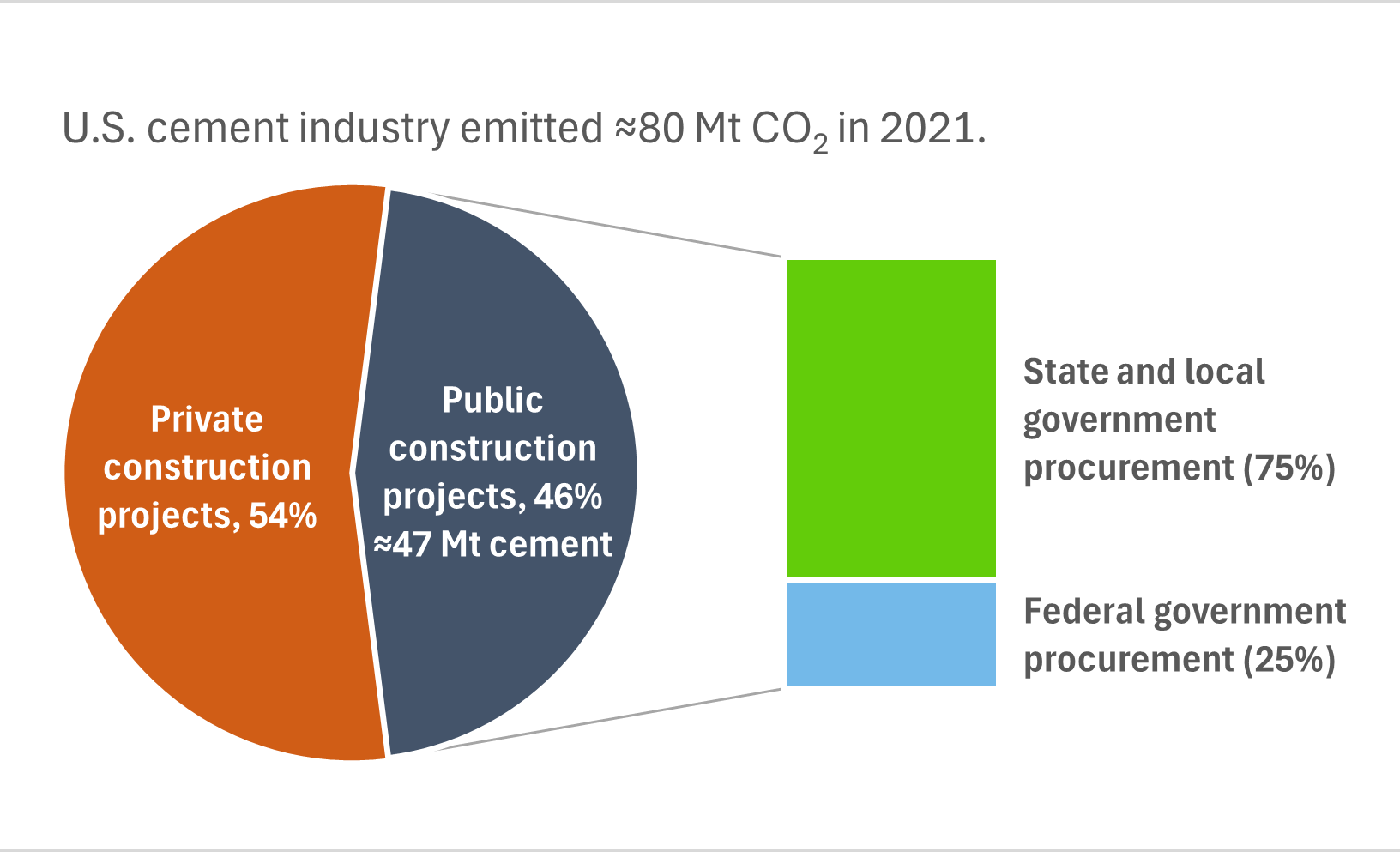

Of the total amount (110Mt) of cement consumed (produced and imported) in the United States, 46% was used in public construction projects (PCA 2016), (i.e., about 47 Mt of cement). Three-quarters (75%) of public procurement is from state and local governments, with the remaining 25% from the federal government (Hasanbeigi and Khutal 2021). The U.S. cement industry emitted around 80 Mt of CO2 in 2021 (calculated based on data from the U.S. Geological Survey (USGS) 2023 and U.S. Department of Energy (DOE) published in 2022).

Figure ES-1. Share of cement consumption between private and public construction projects. Source: PCA 2016; USGS 2024, 2023; DOE 2022.

We conducted a scenario analysis using four scenarios to describe the adoption rate of limestone calcined clay cement by government and private cement users in the U.S. market in 2021—low (10% adoption across the market), medium (20%), high (30%), and transformative (50%)—and estimate the carbon reduction potential for each scenario. Even higher adoption rate scenarios may be possible based on market conditions over time. Based on this analysis, U.S. government (federal, state, and local) purchases of cement for construction can result in the emission reductions presented in Table ES-1.

Table ES-1. Summary of CO2 reduction potential of limestone calcined clay cement used by government procurement in the United States

Limestone calcined clay cement market adoption rate | |||||

| None (Business as usual) | Low (10%) | Medium (20%) | High (30%) | Transformative (50%) |

Annual CO2 reduction potential from government procurement only (Mt CO2) | 0 Mt CO2 | 1.5 Mt CO2 | 2.9 Mt CO2 | 4.4 Mt CO2 | 7.3 Mt CO2 |

CO2 emissions of the U.S. cement industry in 2021 avoided from government procurement only (%) | 0% | 2% | 4% | 6% | 9% |

Equivalent to avoiding CO2e emissions from number of gasoline-powered cars driven for one year (EPA 2024) | 0 | 357,003 | 690,205 | 1,047,208 | 1,737,413 |

Assumptions:

- A 45% replacement rate of limestone calcined clay cement in portland cement, which leads to a 40% lower carbon intensity for limestone calcined clay cement compared to portland cement (business as usual).

- Represents only government (federal, state, local)-procured concrete (46% of total procurement, the rest being mediated by the private sector).

- Market adoption rates in each scenario of 10%, 20%, 30%, 50% create a range of emissions reductions based on level of adoption from low to transformative.

- Estimates only emissions reductions due to material efficiency, not improvements in energy efficiency or use of clean energy for electrical processes (e.g., grinders, calciners).

Limestone calcined clay cement, a blended cement, produced by fossil fuel-based conventional calciners offers a 40% reduction in emissions over conventional portland cement. Electrification of the clay calciner, when powered by renewable energy, can help produce zero-emission calciner clay. If this zero-emission calcined clay is used in limestone calcined clay cement production, then the emissions reduction can be as high as 50%.

According to the U.S. Department of Energy (DOE) Pathways to Commercial Liftoff: Low-Carbon Cement report, electrification of precalciner/kiln technologies used in conventional portland cement production may achieve up to a 35% reduction in carbon emissions (Goldman et al. 2023). Thus, if clinker is also produced by an electrified precalciner/kiln using renewable or clean process heat and is coupled with zero-emission limestone calcined clay, then the limestone calcined clay blended cement would achieve about 70–75% emissions reduction compared to conventional portland cement.

Maturation of the calcined clay technology over time to include higher than 45% replacement rates in blended cement and concrete mix design efficiencies can further bring the total emissions reduction potential to 80% or higher in zero-emissions scenarios (compared to business as usual). Carbon capture, utilization, and storage (CCUS) can then be employed to reduce emissions further. These estimates underscore the importance of advancing research, development, demonstration, and commercial deployment of electrification technologies for the cement sector through the Inflation Reduction Act (IRA 2022), the Concrete and Asphalt Innovation Act (2023), and other policy initiatives.

Advancing such opportunities in the United States showcases American leadership in green manufacturing and demonstrates how innovation can transform this sector in other large cement-producing countries like China and India and globally.

Governments, cement companies, concrete companies, and the NGO community can help overcome barriers and increase adoption.

Barriers to adoption of calcined clays as an SCM in concrete and in a blended cement like limestone calcined clay cement include:

- Technical barriers: End users require their cement to maintain adequate mechanical properties and performance. While this has been demonstrated at lower replacement rates (40% and under), additional studies are required for replacement rates of limestone calcined clay cement in a portland blended cement higher than 50%. For example, additional studies and pilots are required to address reduced early age compressive and flexural strength of limestone calcined clay cements compared to portland cement in construction applications.

- Codes and standards: Limestone calcined clay is already covered in the ASTM International Standards C595, C595M, and C618. However, its application in the United States has been limited because of historical construction practices and insufficient production and suppliers in the country. In addition, existing industry standards and codes do not account for the higher replacement rate of calcined clays (40% currently allowed) or limestone (15% currently allowed) in limestone calcined clay cement (the blended cement) or calcined clays as an SCM in concrete (15% currently allowed).

- Policy barriers: There are no specific policies, regulations, or incentives for low-carbon cement alternatives, nor do all procurement policies consistently prioritize low-carbon options. This is partially due to the lack of awareness and understanding of the benefits of limestone calcined clay cement among policymakers and industry stakeholders.

- Market barriers: Barriers include, for example, the limited market penetration rate in replacing portland cement with limestone calcined clay cement, the fact that not all parts of the cement and concrete value chain are working to support adoption of limestone calcined clay cement, and the lack of training and practice guidelines for ready-mix operators (who represent the bulk of the market) to use limestone calcined clay cement. Generally, 70% to 75% of sales are made to ready-mixed concrete producers, 11% to other concrete product manufacturers, 8% to 10% to contractors, and 5% to 12% to other customer types.

To overcome barriers to the implementation of limestone calcined clay cement, we recommend the following:

- Build supply by increasing financial support. Producers should invest in cement production technology by upgrading or constructing new manufacturing facilities to raise manufacturing capacity. Government policies should create tax breaks such as accelerated depreciation for manufacturing equipment and a tax credit for material production.

- Accelerate research, testing, and demonstration. Industry, academia, and state governments should advance research and development; accelerate testing to improve performance, viability, and compatibility with concrete mix designs; conduct performance trials to boost product legitimacy and market confidence; support pilot and demonstration projects to test scenarios (e.g., in colder climates) and update state department of transportation (DOT) specifications; and share success stories through case studies to highlight viability and advantages.

- Prioritize policy and standardization actions. Governments should update or establish procurement and other policies to promote use, create markets, and set emissions-reduction goals. Governments and market entities should revisit existing cap and trade/invest policies to incorporate reduction potential from energy efficiency and electrification powered by clean energy from new technologies. The standards community should update standards and certification procedures to allow for more flexibility in limestone calcined clay cement replacement levels, performance requirements, and SCM substitution rates in concrete. Industry and the codes community should promote the use of limestone calcined clay cement in building codes and state DOT material specification lists.

- Educate the market and policymakers. Industry can offer technical assistance, training, and resources to customers. It can work with NGOs to educate end-users of cement, such as architects, engineers, developers, and public building owners, about limestone calcined clay cement and its environmental and climate advantages.

- Value collaboration and integration. To enable wider adoption, stakeholders should create partnerships with suppliers and contractors and create dependable supply chains and product availability at the right cost, promoting the use of calcined clays in construction projects. Industry and the architect and engineering communities can collaborate with governmental organizations to create policies that encourage use of calcined clays in construction, comment on proposed regulations, and leverage available technical resources. Governments can cooperate with industry stakeholders to promote calcined clays and aggregate demand.

- Work with local communities. NGOs can spread awareness of air quality and public health benefits.

| Suggested Citation |

| Hasanbeigi, Ali, Pavitra Srinivasan, Hellen Chen, and Nora Esram. 2024. Adoption of Limestone Calcined Clay Cement and Concrete in the U.S. Market. Washington, DC: ACEEE and GEI. www.aceee.org/research-report/i2401 |

This Article Was About

Emerging Technologies Government Lead by Example Efficiency Potential Federal Industrial Policy Embodied CarbonAuthors