Key findings

|

Medium- and heavy-duty vehicles (MHDVs) are essential to the U.S. economy, delivering everything from consumer goods to raw materials and agricultural products to ports, stores, factories, and homes. MHDVs produced 23% of transportation greenhouse gas emissions in 2022, and over half of on-road nitrogen oxide and direct particulate matter 2.5 (PM2.5) emissions, despite only representing 4%–6% of the on-road fleet. Growing freight activity in the United States means that greenhouse gas emissions from MHDVs have grown 76% from 1990, more than three times the growth rate of on-road vehicle emissions overall.

In 2024, the Joint Office of Energy and Transportation, the U.S. Department of Energy, Department of Transportation, and the Environmental Protection Agency released the National Zero-Emission Freight Corridor Strategy (NZEFCS or Freight Corridor Strategy) to “catalyze public and private investment; and support utility and regulatory planning and action at local, state, and regional levels.” The Freight Corridor Strategy took a technology-neutral approach by considering both battery electric and hydrogen fuel cell electric MHDVs. Through a four-phased framework, the Freight Corridor Strategy identified priority hubs and corridors of a nationwide zero-emission freight network with consideration for freight volumes, communities disproportionately impacted by poor air quality, supportive state policies, and other factors. The defined network was then used to help inform the investment decisions of key federal funding streams including the Clean Port Program, Charging and Fueling Infrastructure Funds, and Clean Heavy-Duty Vehicles grant program.

The absence of follow-on federal guidance, as well as policy and funding reversals, have shifted responsibility for implementation of zero-emission freight corridors to states willing to take the lead as well as corridor coalitions, utilities, and the private sector. This report builds on the NZEFCS by assessing the future needs of a key subsegment of MHDVs that require greater coordination between states: regional and long-haul trucks operating daily trips of 200 miles or more. Longer distance trips are more likely to be affected by fragmented or patchwork investments across key corridors and require advance planning.

To avoid fragmentation, the key challenge in building out a nationwide zero-emission freight network is to determine how best to sequence investments to balance near-term benefits, cost, and risk. Comparing battery electric trucks and hydrogen fuel cell trucks reflects the current state of commercially available zero-emission trucking options, while acknowledging that technologies will continue to evolve.

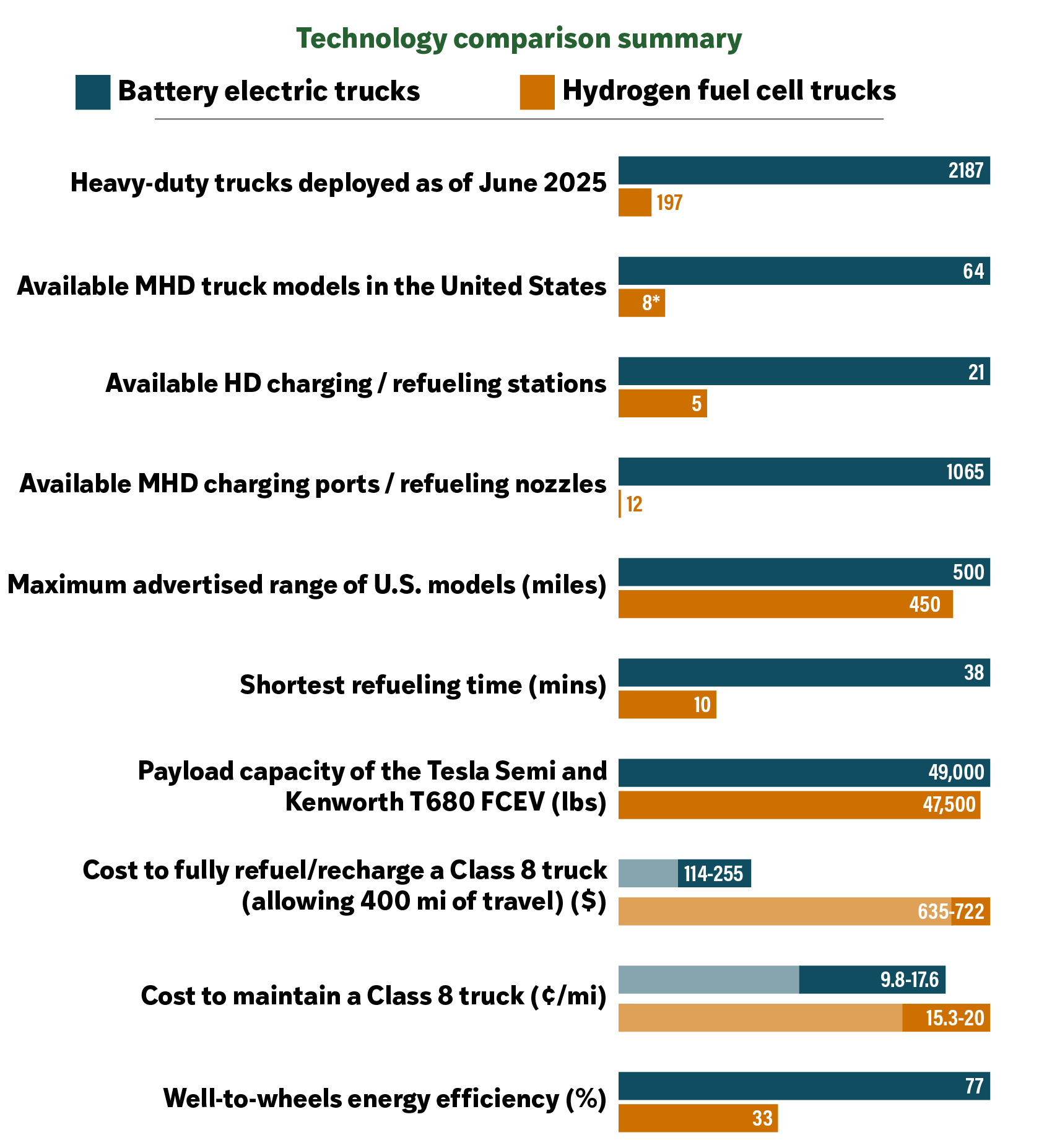

*Only two fuel cell truck models are commercially available.

Figure ES1. Market and technology comparison of battery electric and fuel cell trucks. Sources: Richard et al. 2026; CALSTART 2025, 2026; Alternative Fuels Data Center n.d.; Tesla n.d.; Hyundai n.d.; Windrose n.d.; Brasher 2024; Daimler Truck 2023; Konstantinou et al. 2025; Basma et al. 2023; Bennett et al. 2022; Hunter et al. 2021; Unterlohner and Earl 2020; Tsakiris 2019.

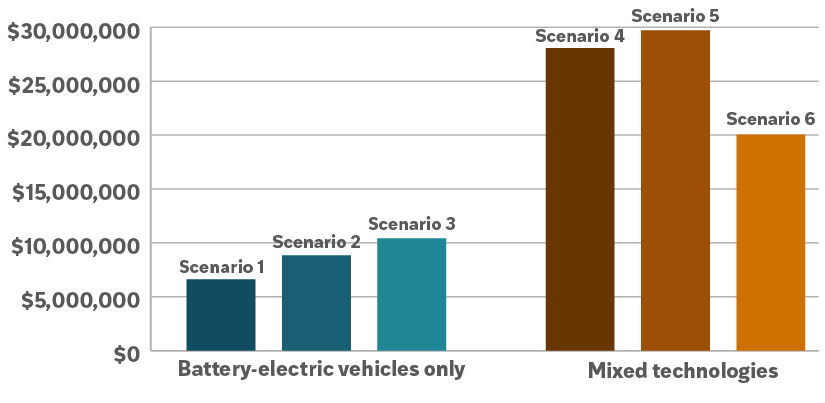

In addition to providing a summary of the operating conditions and state of technology for battery electric trucks and hydrogen fuel cell trucks, ACEEE also estimates the cost to build out a nationwide public and semi-public refueling network for hydrogen fuel cell and electric trucks along major freight corridors. The six scenarios included in the analysis were developed to examine the cost implications of policy choices around ZEV infrastructure even with some uncertainty about how these technologies will evolve, adoption timelines, and to precisely what extent each technology will depend on public versus private refueling infrastructure. In all examined scenarios, we assume that by 2040, 95% of Classes 4–8 trucks sales are ZEVs. With our applied fleet turnover assumptions, this equates to 35% of on-road trucks in 2040 being ZEVs. For more detail on our approach and methodology, see Appendix A.

Scenario 1: Battery electric vehicle (BEV) (baseline public charging) Assumes 100% of ZEVs are battery electric trucks across all weight classes with a lower share of charging occurring at public or semi-public stations: 20% of energy demand for Classes 4–6 trucks and 60% for Classes 7–8 trucks. | |

Scenario 2: BEV, public charging+ Assumes 100% of ZEVs are battery electric trucks, with a higher share of charging occurring at public or semi-public stations: 30% of energy for Classes 4–6 trucks and 80% for Classes 7–8 trucks. This scenario reflects greater reliance on public and semi-public charging infrastructure.

| |

Scenario 3: BEV, public charging++ (test case) Assumes 100% of ZEVs are battery electric trucks across all classes and 100% of charging occurring at public or semi-public stations. This scenario provides an upper-bound estimate of public infrastructure needs and costs and is used to assess maximum cost exposure. | |

Scenario 4: Mixed (baseline public charging) Introduces limited fuel cell adoption in heavy-duty applications, with 20% of Classes 7–8 ZEV trucks using hydrogen fuel cells and all other ZEV trucks battery electric. Public charging shares for electric trucks are the same as in scenario 1, isolating the effect of technology mix. | |

Scenario 5: Mixed, public charging+ Combines limited fuel cell adoption in Classes 7–8 ZEV trucks (20%) with higher public charging reliance for electric trucks, matching the assumptions in scenario 2. | |

Scenario 6: Mixed technologies, extended hydrogen station spacing (test case) Follows the assumptions of scenario 5 but alters the minimum spacing requirement for hydrogen refueling stations so that it is at a constant 200 miles for the entire period of analysis. This scenario provides a lower-bound estimate of infrastructure needs and costs for hydrogen refueling infrastructure. |

Building out a public refueling network for battery electric and fuel cell electric trucks requires substantial investment, but the costs of station development associated with each fuel type differ markedly. The costs to build sufficient hydrogen refueling stations are considerably higher than the cost to build sufficient charging stations. As a result, scenarios with both technologies considered in the fleet mix (scenarios 4–6) have the highest overall system costs.

Figure ES2. Total station investment cost, 2025–2040 ($000). Source: ACEEE.

Zero-emission freight corridors will only succeed if states plan and invest beyond their own borders. Coordinated action on station siting, deployment timelines, and funding strategies is essential to create continuous, usable networks and avoid fragmented, high-cost infrastructure. As battery electric truck technology continues to improve, including the recent introduction of longer-range semi models entering the market, poor coordination and delayed infrastructure deployment risk becoming a binding constraint on adoption. Early preparation of ZEV-ready sites and alignment with utility proactive planning can significantly shorten deployment timelines, reduce future upgrade costs, and preserve flexibility as freight demand grows.

In the near term, battery electric charging represents the lowest-risk and most mature investment pathway and should form the backbone of early corridor development. Charging technology is commercially proven and aligns with existing grid planning processes. In contrast, hydrogen refueling technology remains less developed, significantly more expensive, and dependent on uncertain fuel supply and demand dynamics. It is unclear whether hydrogen infrastructure will advance quickly enough to match the pace and reliability of battery electric systems. As a result, hydrogen investments should proceed cautiously through phased, demand-tested approaches to avoid stranded, underutilized assets.

View the webinar here:

Download the research report

| Suggested Citation |

| Aland, Rachel, Peter Huether, and Christi Nakajima. 2026. Pathways to Zero-Emission Freight: Infrastructure Needs for Regional and Long-Haul Trucking. Washington, DC: ACEEE. aceee.org/research-report/t2601. |