Key findings

|

Electrification of current fossil fuel end uses and a low-carbon electricity supply constitute the most proven approach to reducing greenhouse gas (GHG) emissions, particularly for buildings. Alternative fuels (a category of fuels that can be used instead of fossil fuels, including biofuels, hydrogen, and synthetic fuels) may provide a path to reducing emissions in hard-to-decarbonize sectors such as long-distance transportation, high-temperature industrial processes, load-following electricity generation (generation that can adjust power output to match fluctuating electricity demands), and certain thermal demands in buildings, such as space and water heating in cold climates. In this report, we survey potential supply and hard-to-decarbonize demands across sectors before a detailed analysis of building end uses.

A systematic analysis considers alternative fuels in the context of economy-wide decarbonization

In this report, we take a systematic approach to assess how alternative fuel supply and demand might develop, and what role alternative fuels might play in decarbonizing buildings in the context of other sectors. We evaluate potential integration challenges and how uses of alternative fuels might be prioritized. Finally, we consider policy options that could affect the alternative fuels market and fuel distribution across sectors.

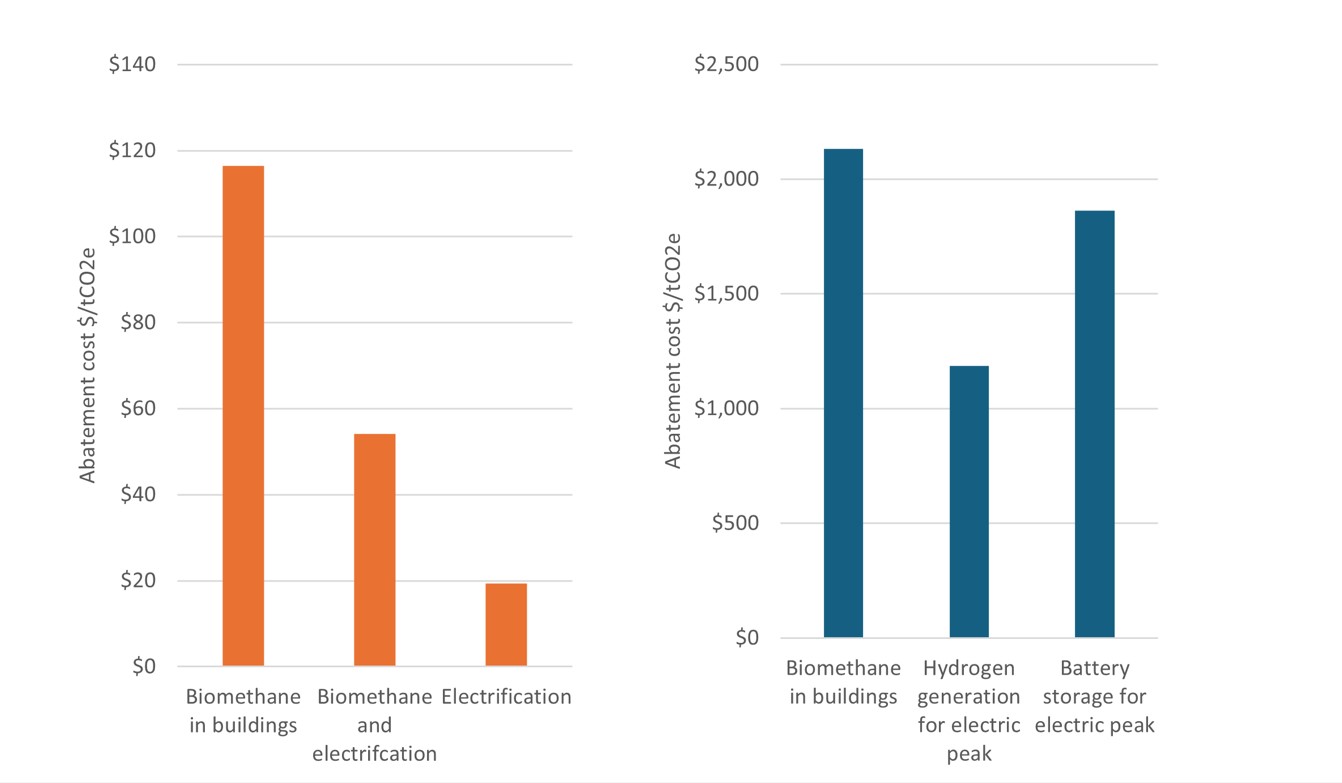

We assessed the possibility of using alternative fuels to decarbonize buildings through an analysis of scenarios illustrative of potential market developments. We constructed scenarios with varying use of alternative fuels and electrification for hard-to-decarbonize building end uses. For each case, we calculated emissions, cost, and abatement cost, compared to a baseline where natural gas is used for hard-to-decarbonize energy demands. While biomethane used directly in buildings could be a viable decarbonization measure, electrification has a greenhouse gas emissions abatement cost six times lower (figure ES 1(a)). Regional variability exists in both the current electrical grid emissions factors and the pace of grid decarbonization. Yet the scale of the difference in figure ES 1(a) suggests electrification is likely to be the preferred general approach across the United States, even if local conditions may lead to some combining of electrification and biomethane in buildings.

We also assessed example peak scenarios for a cold climate region with ambitious decarbonization targets to compare the impact of using biomethane or electricity storage charged by low-carbon generation resources to meet peak heat demand. Here, we found the emissions abatement cost of biomethane in buildings to be only slightly higher than that of grid-scale battery storage. However, a different alternative fuel—hydrogen—was found to be the most cost-effective way to reduce emissions associated with extreme peak electricity demands (figure ES 1(b)).

Figure ES1 (left). Costs of CO2 abatement options for hard-to-decarbonize building end uses

Figure ES2 (right). Costs of options for decarbonizing peak heat demand

Life-cycle emissions of alternative fuels must be evaluated using standardized methods

Life-cycle emissions of biofuels include the emissions associated with production—both increased emissions (e.g., from land-use change or fertilizer use) and carbon dioxide withdrawn from the atmosphere during feedstock growth—as well as emissions associated with burning them for end uses. For hydrogen and synthetic fuels, the emissions vary depending on the production method and, especially in the case of hydrogen electrolysis, the emissions factor of the electricity supply. Any alternative fuel that is a hydrocarbon creates GHG emissions and health-impacting air pollution when combusted. Further, if drop-in alternative fuels are used as natural gas substitutes, then the methane leakage that currently occurs in natural gas transmission and distribution systems would continue to be a significant emissions source, unless steps are taken to greatly reduce leakage throughout the system.

Scale of supply will likely limit the potential roles of alternative fuels

The total supply of alternative fuels is likely to be significantly smaller than current fossil fuel demand in hard-to-decarbonize sectors. Even under optimistic projections for alternative fuels supply, our analysis indicates only 12% of current fossil fuel use, or 64% of hard-to-decarbonize fossil fuel use could be met by alternative fuels. Our analysis also indicates that only in limited scenarios are alternative fuels likely to be more cost effective than electrification. Therefore, end use electrification and low-carbon electricity will likely remain the cornerstones of economy-wide energy decarbonization.

Hard-to-decarbonize end uses in transportation, industry, and power generation may be better uses of alternative fuels

There are limited alternative solutions for decarbonizing energy sectors with technological barriers to electrification: long-distance or heavy transportation, high-temperature industrial processes, and seasonally varying electricity generation (IRENA 2024; Finkelstein, Frankel, and Noffsinger 2020). Prioritizing these energy demands for alternative fuels will likely result in lower emissions and costs than directing significant use of this limited fuel supply to buildings.

The best approach to hard-to-decarbonize building end uses will depend on how biomethane supply evolves

Biomethane combined with electrification could decrease emissions from the 8% of current building fossil fuel usage that we classify as hard to decarbonize (e.g., cold climate peak space heating demands and central water heating in large multifamily buildings) at abatement costs below the EPA’s computed social costs of greenhouse gas emissions (U.S. Environmental Protection Agency 2023). However, we find that electrifying these energy demands could further reduce emissions at a lower abatement cost than biomethane: In other words, biomethane is unlikely to generally be a preferred approach even for end uses that are more challenging to electrify. Leaks from gas infrastructure can contribute significantly to life-cycle emissions in any scenario that requires maintaining the gas system. Since methane is a more potent greenhouse gas than carbon dioxide, any decarbonization strategy that includes utility delivery of natural gas or alternative fuels via existing natural gas infrastructure must also prioritize reducing gas leakage. However, significant costs are associated with reducing gas leakage, especially when any economy-wide decarbonization scenario is likely to significantly reduce gas sales to recover those investments.

Alternative fuels may also support building decarbonization through load-following electricity generation

Electrifying building heating demands will result in significant increases in electric peaks in moderate-to-cold climates. Using biomethane as a secondary heat source in buildings could reduce the electricity supply necessary to meet peak heat demands. Also, low-carbon hydrogen could provide long-duration energy storage and electricity generation to meet larger electrification-driven peak demands. Both examples illustrate how combining electrification and alternative fuels can advance decarbonization.

Policy measures can drive market growth of efficient alternative fuel solutions

Renewable fuel standards have been prominent policy drivers for alternative fuels in transportation, supporting rapid growth in biofuel production. More recently, growing consideration of clean heat standards could provide a similar model for driving growth in building decarbonization, including alternative fuels. Policy measures such as these can influence how the market for alternative fuels develops for specific sectors or fuel types. Other policy measures, such as carbon pricing, could contribute to growth in use of alternative fuels across sectors.

Download the report

| Suggested Citation |

| Traynor, Elizabeth and Michael Waite. 2025. The Potential for Alternative Fuels in Building Decarbonization. Washington, DC: ACEEE. www.aceee.org/research-report/b2503. |